8 Point EOFY Checklist

As we lead in to the End of Financial Year (EOFY), Carey Group has curated its 8 point checklist to help you prepare and utilise any Government approved extensions or amnesty as a result of COVID-19.

You can also listen to these tips on the Carey Group Resilience Series Podcast here.

- Pay the super

- Do this now to claim a tax deduction this financial year. Superannuation paid after the end of the year is not eligible for a deduction until the next financial year. Super must be received by the fund before the end of the year to be tax

- If you have more than the current quarter outstanding, contact your advisor as soon as possible to discuss an action plan to resolve – there is a super penalty amnesty available until September

2. Get the invoices, bills and paperwork

- Invoice out any completed work.

- Chase up overdue and unpaid invoices.

- Write off bad debts.

- Enter into your file any unpaid accounts payable at the end of the month.

3. Reconcile, reconcile, reconcile!

- Reconcile all bank accounts used in the business including credit cards, loans and transaction accounts.

- Clear out ‘suspense’ account – ask your advisor where these items need to go.

- Chase up un-deposited and stale cheques – consider cancelling these cheques and transferring payment via electronic methods.

- Collate PDF copies of bank statements at 30 June and email them to your accountant.

- If the bank account doesn’t reconcile – call your advisor for assistance to correct it.

4. Stock on hand and work in progress.

- Do a physical count of the stock, note the date and time.

- Determine its value.

- Note for your advisor the quantity, type and whether the value includes GST.

- What is the value of the work in progress – work partially completed which expenses have been incurred on.

5. Fixed Assets

- Check the depreciation schedule in your financials.

- Note anything which is no longer on hand and advise.

- Collect up invoices for capital purchases made throughout the year, ready for tax work.

6. Payroll

Single Touch Payroll, JobKeeper and other wages incentives available this year may make the reconciliation of payroll the most important job in June and July.

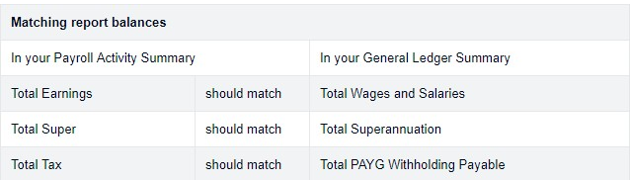

- Run your payroll reports and compare them to your profit and loss accounts – do they match?

- Wages and Salaries in the profit and loss should match the payroll gross wages and allowances total.

- PAYG withheld and Superannuation liability accounts – Balance sheet liability should only be the amount unpaid at balance date.

- Superannuation expense in the profit and loss should match the superannuation total in the payroll report.

- Prepare finalisation summaries (the old group certificate)

- Check employer details are all completed and correct.

- Review employee information and ensure accuracy.

- Confirm all wages to be paid for the year have been processed. Payroll reports use the payment date of each pay run, not the pay period ending date. For example, if a pay period ended on 31 July, but pay day was 2 August, you'll see it on reports for

- Compare the payroll activity summary to the general ledger accounts of wages, paygw and super to confirm all

- If not opted into Single Touch Payroll, prepare the payment summary,

- Check the financial year

- Check all employees listed in the payroll summary report are listed

- Check employee payroll earnings information matches the payment summary.

- Finalise the payment summaries, and submit the annual payment summary report to the ATO (if opted into Single Touch Payroll, check steps 1-3 above, then refer to your specific software to follow the instructions to lodge the finalisation information for your employees).

7. Finally

- Run the profit and loss –

- Does this look right?

- Is there a profit or a loss?

- Run the balance sheet –

- Have my net assets increased or decreased?

- Is there large amounts of money in accounts receivable or accounts payable?

- Gather up the bank statements, capital purchases invoices, stock on hand values and send to your accountant.

8. Make a conscious decision to do something different for the new financial year.

- Have a new financial year financial health check with your accountant – focus on methods for collection of cash for uncertain times ahead – CASH IS KING!

- Draw up a budget for the new financial year – how long can I extend my cash reserve?

- What is your strategic plan? This reflects the objectives you, as the business owner have for your business and your personal life.

- Prepare a cash flow forecast – does your cash flow align with your budget and goals?

- A marketing plan may improve your cash flow if done well – is there an opportunity to increase revenue? Do you need a brand refresh? How can you make your website work harder for you?

- Go digital – financial information is so much easier use when software and tech is used – small changes can make big impact to manual processes and the bottom line.

This article was supplied by Carey Group.